Why High-Net-Worth Retirees Are Moving to Separately Managed Accounts and Direct Indexing

A Custom Approach to Investing for Retirement

Many retirees spend decades diligently saving into 401(k)s, IRAs, and brokerage accounts. By the time retirement arrives, they often discover they have accumulated substantial wealth—but also substantial complexity.

Over the years, accounts become filled with dozens of mutual funds, overlapping ETFs, legacy holdings, concentrated stock positions, and taxable gains. What once seemed like diversification can evolve into a confusing collection of investments that may not be working together efficiently.

For high-net-worth retirees, particularly those with significant assets outside of retirement accounts, simplicity and tax efficiency become increasingly important. The question is no longer simply, "What investments should I own?" Instead, it becomes, "How do I organize my wealth in a way that gives me greater control, reduces taxes, and simplifies my financial life?"

This is where Separately Managed Accounts (SMAs) and direct indexing can provide meaningful advantages.

The Limitation of Traditional Mutual Funds and ETFs

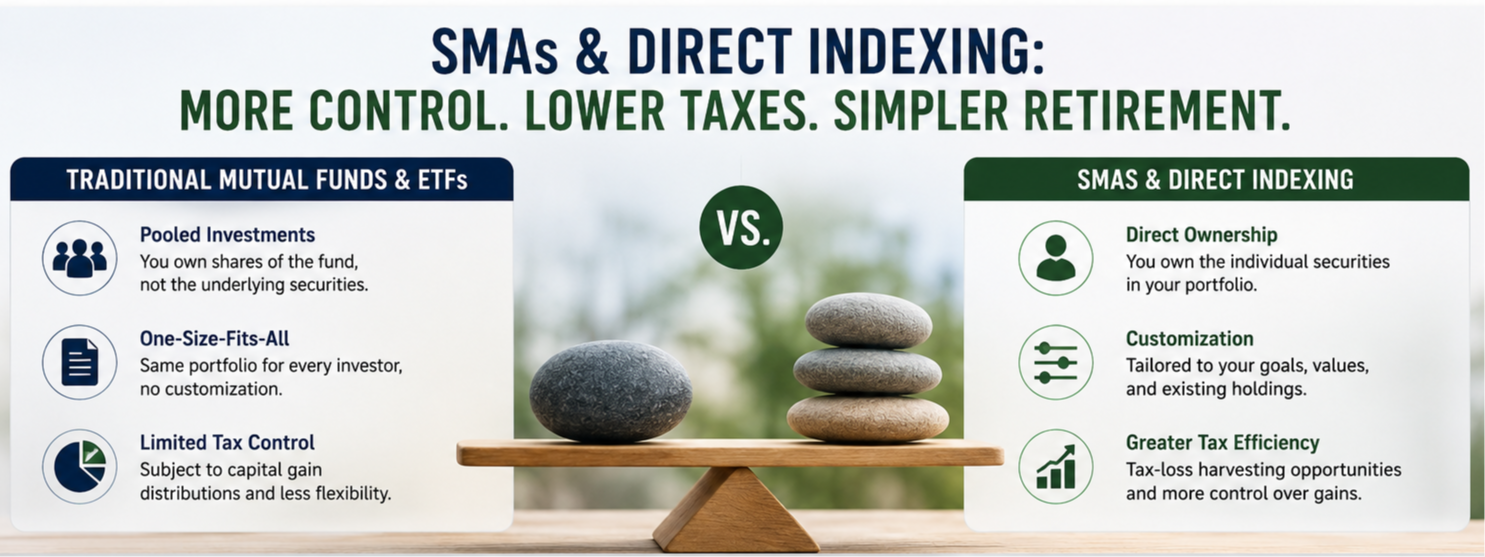

Mutual funds and exchange-traded funds (ETFs) have served investors well for decades. They offer diversification, professional management, and relatively low costs.

However, these vehicles share one important characteristic: they are pooled investments.

When you purchase a mutual fund or ETF, you do not directly own the underlying securities. Instead, you own shares of the fund itself. Every shareholder receives the same portfolio, regardless of their individual tax circumstances, legacy goals, charitable intentions, or personal preferences.

In many cases, this "one-size-fits-all" approach works reasonably well. But for retirees with substantial taxable assets, complex tax situations, or unique investment preferences, it may leave opportunities on the table.

As wealth grows, investors often need a more customized solution.

What Is a Separately Managed Account (SMA)?

A Separately Managed Account is a professionally managed portfolio in which the investor directly owns the underlying individual securities rather than owning shares of a pooled fund.

Instead of purchasing a mutual fund containing hundreds or thousands of stocks, the investor owns the individual stocks themselves.

This structure provides low cost investing similar to ETF’s and offers several advantages that is particularly valuable for affluent retirees.

Direct Ownership and Transparency

With an SMA, investors know exactly what they own.

Rather than seeing only a fund ticker on a statement, retirees can view each individual company held within the portfolio. This creates a level of transparency and control that simply is not available in pooled investments.

Investors may choose to restrict certain industries, avoid specific companies, or customize holdings to align with personal values or existing concentrated positions.

For example, an investor who already owns significant shares of Apple through employer stock compensation may prefer not to add additional Apple exposure inside the managed portfolio. An SMA allows that customization.

Direct Indexing: Taking Customization Even Further

Direct indexing builds upon the SMA concept.

Rather than purchasing an ETF that tracks an index such as the S&P 500, direct indexing purchases the underlying stocks that comprise the index. The goal is to closely replicate index performance while creating opportunities for customization and tax management.

The broad market exposure remains similar, but the portfolio is designed specifically for the individual investor. Direct indexing may also allow investors to customize exposures by reducing concentrated positions or limiting exposure to specific sectors or companies that may be dominating an index. For retirees with substantial taxable assets, this customization can be extremely valuable.

The Tax Advantage of Direct Ownership

One of the greatest challenges high-net-worth retirees face is taxation. Direct ownership can significantly reduce the risk of unexpected capital gain distributions commonly associated with pooled investment vehicles. You are no longer subject to capital gain distributions generated by the trading activity of other investors within pooled funds.

High-net-worth retirees with taxable brokerage accounts, often built through years of disciplined savings, stock compensation, inheritances, or business sales often benefit the most from SMA’s more advanced and intentional investing structure.

Direct ownership through SMAs and direct indexing can provide additional tools to manage these tax liabilities.

Tax-Loss Harvesting Opportunities

Tax-loss harvesting involves strategically selling securities experiencing temporary declines in value in order to realize losses that may offset capital gains elsewhere in the portfolio. With direct indexing, every individual stock becomes a potential tax-management opportunity.

For example, if one stock within the portfolio declines while the broader market rises, that position may be harvested to generate a tax loss while simultaneously purchasing a similar replacement security to maintain market exposure.

Research suggests that ongoing tax-loss harvesting may improve after-tax returns for investors in taxable accounts, particularly during periods of market volatility.

For retirees who regularly realize gains from rebalancing, property sales, concentrated stock positions, or business transactions, these harvested losses can become especially valuable.

Enhanced Legacy Planning

Direct ownership can also improve estate planning flexibility.

Highly appreciated securities may receive a step-up in cost basis at death under current law, potentially eliminating embedded capital gains for heirs. Because investors directly own individual securities inside an SMA, advisors can coordinate gifting, charitable strategies, and legacy planning more intentionally.

For retirees focused on leaving a legacy, this additional flexibility can be valuable.

Simplifying Retirement Wealth

Many affluent retirees accumulate investments from multiple employers, advisors, and institutions over decades.

The result often resembles a financial junk drawer.

It is not unusual for us to review portfolios containing:

- Multiple overlapping mutual funds.

- Hundreds or even thousands of duplicate underlying holdings.

- Significant cash positions earning little return.

- Unintended sector concentrations.

- Excessive portfolio turnover.

- Legacy positions purchased years ago with no current strategy.

- Higher taxes from incorrect allocations

One of our primary goals at Guided Seasons Wealth Advisors is helping retirees simplify.

Rather than owning dozens of overlapping funds, many clients benefit from consolidating investments into a coordinated collection of professionally managed SMA strategies.

This can create:

- Greater portfolio clarity.

- More efficient tax management.

- Easier income distribution planning.

- Improved risk oversight.

- Better coordination with estate and legacy goals.

Simply put, fewer moving pieces often lead to greater peace of mind.

Why Guided Seasons Uses Orion and TownSquare

At Guided Seasons Wealth Advisors, we believe retirees deserve institutional-level portfolio management combined with personalized planning.

That is why we partner with Orion Portfolio Solutions and TownSquare Capital.

Through Orion's technology platform and TownSquare's professionally managed investment strategies, our clients gain access to sophisticated SMA and direct indexing solutions that historically were available primarily to institutional investors and ultra-high-net-worth families.

However, technology alone is not enough. The real advantage comes from combining these sophisticated investment solutions with ongoing human oversight.

Our relationship with Orion and TownSquare provides access to a dedicated trading and portfolio management team that actively oversees implementation.

This creates several important benefits for our retirees:

1. Personalized Tax Management

Having your own trading team that skillfully implements your tax-loss harvesting opportunities, manages gains, and implements transitions more efficiently creates a better overall experience for high net worth clients.

2. Coordinated Rebalancing

Portfolios can be rebalanced strategically while considering income needs, tax planning implications, and maturing positions rather than simply relying on pooled investments without regard to consequences.

3. Transitioning Legacy Holdings

Many retirees arrive at retirement with appreciated securities that grew over decades or stock incentives they obtained during employment. Highly concentrated positions also create highly concentrated risk profiles that need adjustment.

Rather than forcing wholesale liquidation and triggering unnecessary taxes, positions can often be transitioned gradually and thoughtfully through the expert guidance of your personal trading team coordinated by your advisor.

Household-Level Coordination

Accounts across a household can be viewed and coordinated collectively to reduce overlap, improve asset location, reduce taxes, clarify tax planning solutions, and strengthen income planning.

In addition, Orion’s software allows us to create different sleeves of investments inside the same account and track them individually. For example, one portion of an account may be designated for near-term retirement income, while another portion remains invested for long-term growth. This additional clarity can simplify retirement spending decisions and improve accountability.

Who May Benefit Most from SMAs and Direct Indexing?

Although these strategies are not appropriate for everyone, they may be especially beneficial for retirees who:

- Have significant taxable brokerage assets.

- Hold highly appreciated securities.

- Desire greater tax planning efficiency.

- Need customized investment restrictions.

- Want to simplify multiple legacy accounts.

- Wish to coordinate investments with estate and charitable planning.

- Have complex retirement income needs.

For investors with substantial taxable wealth, the difference between pre-tax and after-tax returns can be significant over time.

After all, it is not simply what you earn that matters.

It is what you keep.

Final Thoughts

ETFs remain excellent investment tools and continue to play an important role in many portfolios.

However, for high-net-worth retirees seeking greater flexibility, customization, transparency, and tax efficiency, Separately Managed Accounts and direct indexing may provide meaningful advantages.

At Guided Seasons Wealth Advisors, our goal is to help retirees simplify their financial lives while coordinating investments, taxes, retirement income, and legacy planning into a unified strategy.

Because retirement is not just about building wealth.

It is about preserving it, using it wisely, and creating financial peace of mind through every season of life.

If you have accumulated significant taxable assets and would like to explore whether SMAs or direct indexing could improve your retirement strategy, we would welcome the opportunity to have a conversation.

References

- Cremers, K. J. M., & Petajisto, A. (2009). How Active Is Your Fund Manager? A New Measure That Predicts Performance. Review of Financial Studies, 22(9), 3329-3365.

- Morningstar. (2024). Direct Indexing Landscape Report.

- Morningstar Manager Research. Separately Managed Accounts: Benefits and Considerations.

- Vanguard Research. Putting a Value on Your Value: Quantifying Advisor's Alpha®. 2022.

- Morningstar. (2023). Tax-Efficient Portfolio Construction in Taxable Accounts.

- CFA Institute Research Foundation. Managing Taxable Portfolios.

- Parametric Portfolio Associates. The Potential Benefits of Tax-Managed Investing.

- Russell Investments. Tax-Loss Harvesting: Opportunities to Enhance After-Tax Returns.

- Cerulli Associates. The State of U.S. Managed Accounts.

- Orion Portfolio Solutions. Direct Indexing and Personalized Portfolio Management Resources.

- TownSquare Capital. Investment Management and Tax-Aware Portfolio Implementation Resources.