Taking Social Security at 62? The Decision That Could Cost You Six Figures!

One of the most common questions I hear from clients approaching retirement is, "Should I take Social Security as soon as I can?"

For many people, age 62 has become almost synonymous with retirement. After decades of working, it's understandable to think, "I've paid into the system my entire life. Why wouldn't I start collecting as soon as I'm eligible?" After all, beginning benefits earlier means more checks, and on the surface, that seems like a smart financial move.

The reality, however, is that the decision of when to claim Social Security is one of the most important financial choices you'll make in retirement. In some cases, claiming benefits too early can increase lifetime taxes, force substantially larger withdrawals from your investment accounts, and potentially reduce the financial security of a surviving spouse. Over the course of retirement, those decisions can easily cost a family hundreds of thousands of dollars.

Like most planning decisions, there isn't a universal answer. However, understanding how the system works can help you make a more informed decision for your family.

How Social Security Benefits Are Calculated

Your Social Security retirement benefit begins with something called your Primary Insurance Amount, or PIA. This is the monthly benefit you're entitled to receive at your Full Retirement Age (FRA), which for most people today falls somewhere between ages 66 and 67 depending on the year they were born.

The Social Security Administration calculates this amount using your highest 35 years of earnings. Those earnings are adjusted for inflation, averaged together, and then run through a formula established by Congress. In other words, your benefit isn't based on your final salary or your highest earning year. Instead, it reflects a lifetime of work.

Your Full Retirement Age serves as the benchmark against which all early and delayed claiming decisions are measured.

The Permanent Cost of Claiming Early

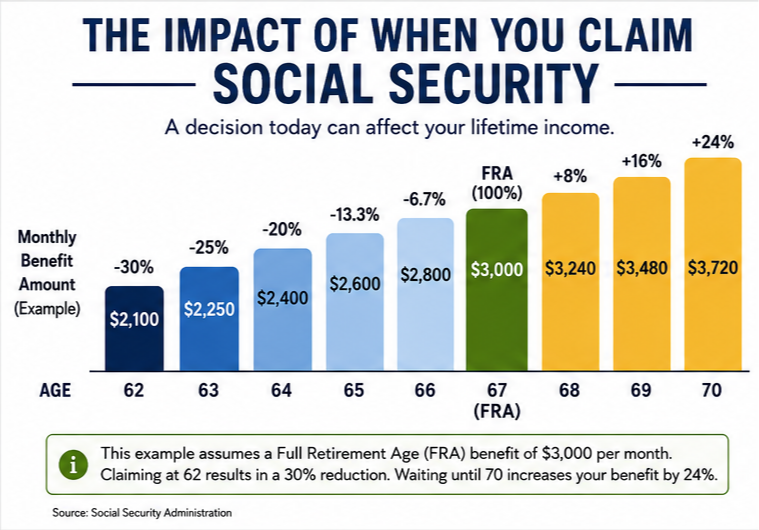

You can begin receiving Social Security benefits as early as age 62. However, doing so comes with a permanent reduction in your monthly benefit.

For many retirees, claiming at age 62 reduces benefits by approximately 25% to 30% compared to waiting until Full Retirement Age. Consider a retiree whose Full Retirement Age benefit is projected to be $3,000 per month. Claiming at age 62 could reduce that benefit to approximately $2,100 per month—a difference of nearly $900 every month for life.

That reduction doesn't disappear when you reach age 67. It continues when you turn 75, 85, and beyond. You are simply receiving a smaller check every month for the remainder of your life.

The question isn't simply, "How soon can I start collecting?" A better question may be, "If one of us lives into our nineties, how much guaranteed income are we willing to give up?"

Many retirees underestimate just how long retirement may last. A healthy couple retiring in their mid-sixties has a very good chance that one spouse will live into their nineties. Over a retirement lasting 25 to 35 years, a permanently reduced benefit can translate into a substantial loss of lifetime income.

The Often-Overlooked Tax Conversation

One area that rarely receives enough attention is the relationship between Social Security, IRA withdrawals, and taxes.

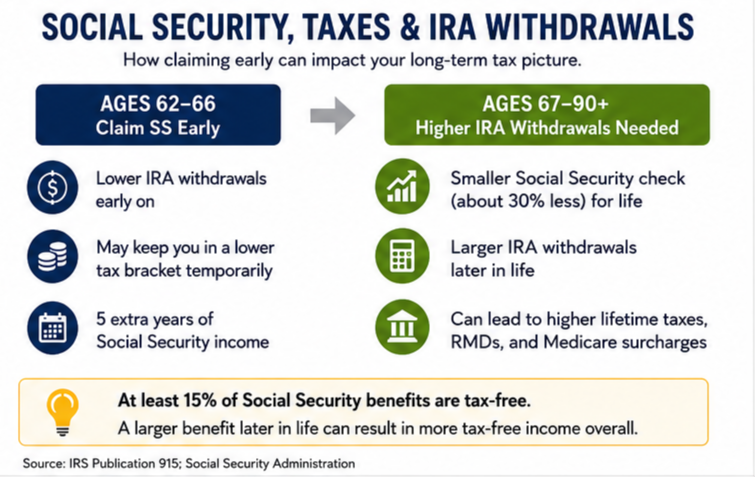

Many retirees assume that taking Social Security early automatically reduces taxes because they are receiving government benefits sooner. In the short term, that may be true. Receiving Social Security at age 62 can allow retirees to take smaller withdrawals from their IRAs during the first few years of retirement.

The challenge comes later.

At a minimum, at least 15% of Social Security benefits are effectively tax-free under current law. Depending on your income level, up to 85% of benefits may be included in taxable income, meaning that a portion of every Social Security payment remains tax-free.

Traditional IRA withdrawals don't work that way. Every dollar withdrawn from a traditional IRA is generally taxed as ordinary income.

Suppose you claim Social Security at age 62. You receive five years of income that may allow you to reduce IRA withdrawals between ages 62 and 67. That sounds attractive on the surface. However, because your Social Security benefit is now permanently reduced by approximately 30%, you may need to withdraw substantially more from your IRA every year from age 67 onward.

Over a retirement lasting thirty years, that difference can become significant. In many retirement projections, a permanently reduced Social Security benefit forces retirees to withdraw hundreds of additional dollars every month from their investment accounts. Over time, this can easily translate into an additional six figures of cumulative IRA withdrawals during retirement.

Those additional withdrawals may lead to:

- Higher lifetime taxes.

- Faster depletion of retirement accounts.

- Larger Required Minimum Distributions later in life.

- Greater exposure to Medicare IRMAA surcharges.

- Reduced flexibility for Roth conversion strategies.

In many retirement plans we build, delaying Social Security while strategically drawing down IRAs or performing Roth conversions during the early retirement years can significantly improve long-term outcomes. This is one reason why Social Security decisions should never be made in isolation. They should be coordinated with your tax strategy, investment plan, and overall retirement income plan.

The Reward for Delaying Benefits

On the other side of the equation, delaying Social Security beyond Full Retirement Age increases your benefit through what are known as Delayed Retirement Credits.

Your benefit grows by approximately 8% per year for every year you delay beyond Full Retirement Age, up until age 70. Returning to our previous example, a retiree with a $3,000 monthly benefit at age 67 could increase that payment to approximately $3,720 per month by waiting until age 70.

That's a 24% increase in guaranteed lifetime income.

Very few investments can provide an inflation-adjusted, government-backed increase of that magnitude. For retirees who are healthy, have longevity in their family, or simply want greater protection against running out of money later in life, delaying benefits can be extremely valuable.

I often tell clients that Social Security is much more than an income source. It is also longevity insurance. The larger your guaranteed income stream, the less pressure there may be on your investment portfolio during difficult market environments or advanced age.

Why Married Couples Need to Think Beyond Themselves

Social Security claiming decisions become even more important for married couples.

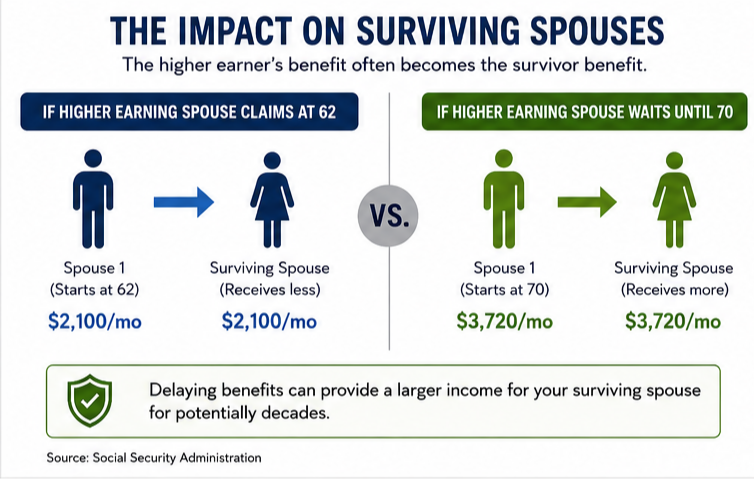

Many people don't realize that the higher earning spouse's benefit often becomes the survivor benefit if one spouse passes away first. This means that when the first spouse dies, the surviving spouse generally keeps the larger of the two Social Security checks.

As a result, if the higher earning spouse claims early and locks in a permanently reduced benefit, that reduction may continue for the surviving spouse for the remainder of his or her life.

I've seen many situations where a widow or widower lives another ten, fifteen, or even twenty years after losing a spouse. Maximizing the higher earner's benefit can provide meaningful financial security during what is often one of life's most difficult transitions.

For this reason, many married couples choose a coordinated strategy in which one spouse claims earlier to provide income while the higher earning spouse delays to maximize future survivor benefits.

Understanding the Earnings Test

Another source of confusion involves working while receiving Social Security.

If you claim benefits before reaching Full Retirement Age and continue working, Social Security may temporarily withhold part of your benefit. For individuals who have not yet reached Full Retirement Age, benefits are reduced by $1 for every $2 earned above the annual earnings limit.

Many people mistakenly believe these benefits are permanently lost. They are not.

Once you reach Full Retirement Age, Social Security recalculates your benefit and gives you credit for amounts previously withheld. Nevertheless, claiming early while continuing to earn substantial wages can create short-term cash flow challenges and may reduce the advantage of claiming early in the first place.

Common Social Security Myths

"I should take Social Security now because the system is going broke."

This concern is understandable, but it is often overstated.

While Social Security does face long-term funding challenges, "running out of money" does not mean benefits disappear. Even if the trust fund reserves were depleted, payroll taxes from millions of American workers would continue flowing into the system and are projected to fund a substantial portion of scheduled benefits.

Historically, Congress has stepped in to make adjustments whenever necessary to preserve the program. Most retirement experts believe reforms will occur long before benefits vanish entirely. Claiming early solely because of fears that Social Security will disappear is rarely the best planning approach.

"I'll take it early and invest the money."

Some retirees certainly can invest early benefits successfully. However, this strategy assumes disciplined investing, favorable market returns, and sufficient longevity to make the strategy worthwhile.

The challenge is that market returns are uncertain, while Social Security benefits are guaranteed for life and adjusted for inflation. For many retirees, maximizing guaranteed income reduces overall retirement risk and provides greater peace of mind.

So When Should You Claim?

The truth is that there is no perfect age for everyone.

A retiree with significant health concerns and limited life expectancy may reasonably choose to claim earlier. A healthy married couple with longevity in their family may benefit substantially from delaying benefits.

Your work plans, tax situation, investment portfolio, legacy goals, and income needs all deserve consideration. Before making a claiming decision, I encourage couples to sit down together and answer a few important questions:

- What is our family history and expected longevity?

- Will either of us continue working?

- How will this decision affect a surviving spouse?

- What impact will this have on taxes?

- How much income do we actually need from our portfolio?

- Could delaying Social Security improve our long-term retirement security?

Social Security is far more than a government check. For many retirees, it is the foundation upon which the rest of retirement income is built. Taking the time to carefully evaluate your options today may provide greater confidence, lower taxes, and significantly more financial security throughout every season of retirement.

Sources

Social Security Administration. Retirement Benefits.https://www.ssa.gov/benefits/retirement/

Social Security Administration. Delayed Retirement Credits.https://www.ssa.gov/benefits/retirement/planner/delayret.html

Congressional Research Service. Social Security: Financing and Trust Fund Solvency.https://crsreports.congress.gov

Internal Revenue Service. Publication 915, Social Security and Equivalent Railroad Retirement Benefits.https://www.irs.gov/publications/p915